Last week I traveled to Atlanta to attend the 44th annual Venture Capital Institute conference. It was a fantastic time filled with some life-changing lessons. My desire to bundle those lessons up into a digestible blog post has delayed my usual timeline a bit, so expect a post on that early next week. In the meantime, I thought I would share one of the most interesting podcasts I have heard in a long time. Fair warning: this podcast has little to do with tech and even walks dangerously close to the line of politics. That being said, I think it is hugely important that people listen to this episode to hear about the very compelling research that Dr. Bjørn Lomborg and his team at the Copenhagen Consensus Center have compiled. Lomborg and a team of Nobel Laureate economists analyzed the UN’s current development goals and force ranked them by capital efficiency. Basically, they looked at for every $1 dollar invested into each development goal, what will the economic impact be. There are a few results that I am sure will surprise you! I love this pragmatic methodology and the way it allows policy makers to more effectively allocate resources. Similar to startups, it turns out that capital efficiency is very important for global development too (had to tie it back somehow!). Enjoy!

Podcast of the Week: Invest Like the Best, EP. 112 - Building Pick and Shovels, with Hunter Walk

I know, I know. I just did an episode from Invest Like the Best. I really wanted to do something from another show this week to maintain some semblance of variety, but this episode was simply too good to pass up. In it, Patrick interviews Hunter Walk about his early stage investment firm, Homebrew, his past experiences working at Google, as Head of Product at Youtube, and on the videogame, Second Life. This episode is chalked full of fascinating stories and actionable insights. I especially loved hearing about how Hunter helped solve copyright issues at Youtube and Hunter’s questions he asks every entrepreneur. Don’t miss this great episode!

Squirrel hunting is a lot like building a startup

A little bit of a stretch, I know, but stay with me here.

Thanksgiving is a BIG deal for my wife’s family. For the past 27 years, they have hosted 30+ people for Thanksgiving dinner (lunch) in their 200+ year old house. We fill the living room with tables and chairs and everyone squats down wherever they can. The menu is pretty outrageous in order to accomodate so many people. This is a far cry from the Thanksgivings I was used to growing up where it would just be the 5 of us in my family up at our cabin in the mountains reading, relaxing, and watching football.

Something else that is different with my wife’s family is Black Friday. I never used to do anything special for Black Friday, but my wife’s family has a very specific set of traditions. Every Black Friday, Caitlyn and her mom will go on and all day shopping spree while the guys of the family go hunting. Now I did not grow up around guns or hunting so the experience of tagging along is all very new to me. This year as we were going squirrel hunting, I was struck by some of the similarities between hunting and starting a successful technology startup. Here are a few things that are comparable.

Squirrel Dog (Market Validation Research)

As with any start up, hunting is a team sport. One of the keys to successfully squirrel hunting is have an aptly named Squirrel Dog. A Squirrel Dog is a dog that is trained to, you guessed it, go find the squirrels. They will go off on their own as you hike around and find the squirrels before “treeing” them by running around the base of any tree with a squirrel barking which both signals they have found something, and keeps the squirrel from running away. I found this behavior very similar to the market validation research that successful companies undertake before even building out a prototype or wireframe. The number one reason why startups fail is due to a lack of market demand for their product or service. By going out of you way you can ascertain exactly where the market opportunity (squirrel) is and devise an appropriate plan of attack.

Gun Choice (Product Market Fit)

Once your dog has treed a squirrel, you need to make sure you are equipped with the right gun for the task. Now I know next to nothing about firearms, but I do know enough to understand that you don’t go squirrel hunting with a .50 caliber rifle. Similarly, it doesn’t matter how perfectly poised for disruption a market is if you don’t have a product that truly addresses the problem people are facing. Now finding product market fit can often be a lot more difficult then picking the right gun for the job, but in either situation picking the wrong tool for the opportunity will leave you unsuccessful.

Taking The Shot (Execution)

Getting the squirrel in your sights with the proper gun is really just the start. If you aren’t able to execute the shot to perfection, it nothing else will matter. In venture, there is a debate on whether a market or a team is really what drives success. There are strong arguments for both, but as a seed-stage investor, I cannot help but believe that the right team is crucial. Even with the more ripe market and the perfectly formulated product, the startup could still be unsuccessful if the team is unable to execute.

Retriever (Business Model)

Assuming you are skilled enough to hit your target, there remains the question of how to extract your prize from the underbrush. You could hike through and get the remains yourself, but this would be a very manual process. Instead, most hunters will use a dog to retrieve for them. For startups, a scalable business model is absolutely essential for any type of meteoric growth. Many processes can be accomplished manually, but without some sort of business model to provide leverage, the company will be hamstrung as they struggle to meet the needs of their customers. Finding product market fit is the first priority for any entrepreneur, but developing a scalable business model is a close second.

Hunting Seasons (Market timing)

Even with the perfect market, an excellent product, a great team, and a scalable business model, you might fail simply because the market is not ready for your solution. Market timing is one of the hardest things for any startup to plan for because it is out of their control and requires founders to adjust opportunistically. You can find example after example of great ideas that failed because the supporting technology was just not there yet. Uber could never have existed before the proliferation of smartphones and GPS technology gave them the ability to put a dispatcher in anyone’s pocket. Other times changes in regulatory requirements can kill a business just as it is taking off. Just ask Juul. Timing is similarly important in hunting. To maintain a sustainable number of animals, hunting is only allowed in very specific seasons. You could face serious repercussions if you are found hunting the wrong animal at the wrong time.

Told you I could (mostly) make it work.

Podcast of the Week: Invest Like the Best, EP. 32 - The Art of Tracking, with Boyd Varty

This episode is from over a year ago, but it is has definitely been one of the most impactful and transformative podcasts I have ever listened to. Invest Like the Best with Patrick O’Shaughnessy is my current favorite podcast and every episode is a must-listen as soon as it is published every week. This particular podcast with Boyd Varty about living the life of a tracker and bringing a restoration mindset to everything you do has made a particular impact on my life. It is the podcast I have shared the most with others and I just finished my third listen through on my drive back to Virginia for Thanksgiving. Be sure to give it a listen and if you are interested in hearing more from Boyd, check out Part II and Part III.

I mentioned that this podcast has had a big impact on me. It has served as an impetuous to adopt a more process/journey focused mindset instead of obsessing about goals and outcomes. Another great resource that has helped shape this mindset is the book Chop Wood, Carry Water. It is a only about 100 pages long, but I am not exaggerating when I say reading it has changed my life for the better. It is another Patrick O’Shaughnessy recommendation and if you would like to read it, you can pick up a copy here.

One-Thousand Thanks

I have always loved Thanksgiving. Great times with family. Lots and lots of great food. And most of all, some time set aside to step back and reflect upon everything you are grateful for in life. My father is Norwegian and one of the common phrases you’ll hear in Norway is “tusen takk”. Tusen takk literally translates to one-thousand thanks and is how a Norwegian might say “thank you very much”. I have always enjoyed the image of someone thanking you emphatically by saying “thank you” one-thousand times over and over again. As I write this post out at my father-in-law’s office (no internet at my wife’s childhood home in rural Virginia. I know, I think it is crazy too, but they really don’t seem to mind), I can’t help but think about the thousand things I have to be grateful for this Thanksgiving season. Here are a few of the things I have been thinking about most.

My Family

I am incredibly lucky to have the family I do. I have the best wife in the world and the past year of our marriage has without a doubt been the greatest year of my life. My family has always been incredibly supportive and they are still always there for me even though we no longer live close to one another. My brothers are my best friends. My dad is my role model. My mom is the rock that holds our family together. I am also so incredibly grateful for my in-laws who have welcomed me into their family with open arms.

My Faith

This isn’t something I talk about a lot on this blog because of its personal nature, but I would be making too big of an omission if I left it out of this post. My faith is the foundation of who I am and it is my guiding light through thick and thin.

Our New Home

My wife and I are so grateful for the new home we have found in Columbus. We have really enjoyed our short time in the city and cannot overstate how much we have felt welcomed with open arms. I had never spent any meaningful time in the Midwest prior to our move, and I have been struck time and time again by the kindness of people living here (and the deliciousness of their food…). It is truly a privilege to be part of such a young, growing city. In Columbus, there is a palpable optimism that is wonderful to be a part of. People here truly believe that tomorrow will be better than yesterday (which is not something that can be said about many parts of our country, especially our previous home, Washington, DC.)

My New Job

The reason I moved my family half-way across the country to a state we had never been before was to take a job as an Analyst at Rev1 Ventures. I took this leap because I wanted to be a part of building the next great tech ecosystem and because I wanted to help support entrepreneurs that were creating truly impactful companies. I couldn’t be happier with the progress I have made so far. There is still a lot of work to be done and I am not anywhere close to accomplishing what I have set out to at Rev1, but I am so grateful for the opportunity I have to work at an organization like Rev1. I am grateful to work alongside some incredible colleagues who all believe in the power for entrepreneurship to fuel the American Dream as much as I do. I am grateful that I have the opportunity to support entrepreneurs that are genuinely trying to change the world. I am grateful that my Sunday evenings are a time of eager anticipation.

You

This blog started out as a tool in my VC-job-search utility belt. It was a way to demonstrate that I was using my free time to be thoughtful about the space. It has become so much more than that to me and I am truly grateful for everyone that takes time out of their day to read through my musings (sometimes ramblings) on the world of venture capital and tech startups. I have been really happy with the cadence I have worked up to and really believe that my writing and analysis improves with every post. Thanks for reading!

These are just a few of the things I am most grateful for. If I really listed out everything that I am thankful for, I would still be working on this post come next Thanksgiving. I know this post is a little bit outside the norm, but I hope that you enjoyed it.

Have a Happy Thanksgiving with you and yours!

What I have learned about negotiation

Han could use some lessons on modern negotiation.

Full disclosure: not much. But I have picked up a few things here and there that I thought were worth sharing.

Put the gun in the other person's hand

I heard this principle on a podcast. I think it is a Mungerism but it could also be a Buffetism. The concept is to let the other person drive your negotiation. Put them in a position of power and just ask them to do what they think is fair. Two reasons for this. One, this can often lead to better outcomes as the person you are negotiating with tries to live up to the trust you have put in them. Two, if they take advantage of the situation to screw you, you now have a crystal clear window into their character and can reevaluate your relationship moving forward. you now have someone you trust to work fairly with you in the future or you have someone who you know is only in it for them selves. Either way you're better off.

Negotiate from the ground up

I take this from a wonderfully simple post from Max Niederhofer on what he has learned about negotiation. I loved this post so much I hung it up on my wall! The strategy is commonly sited in negotiation how-to's, but bear's repeating. The key takeaways are to treat people on the other side of the table like the humans they are and that the more you prepare, the more likely you will get a good outcome. Start by knowing exactly how much you want to buy/sell something for. Then start 35% higher/lower in the applicable direction. Move 20% closer. Then 10% closer. Then 5%. Finally throw in something non-monetary that you have identified earlier that could be seen as a "win" for the other party. The decreasing intervals of this framework will signal you are getting closer to your break point. The kicker at the end will make the other party feel as if they have walked away winners. I very much align with Max’s view that negotiation is not winner take all. The key is to act emphatically and come to a scenario everyone around the table can feel comfortable with.

Make them blink

The most audacious and least widely applicable of the three strategies in this post. I take this from the podcast I highlighted earlier this week with Nick Kokonos. Nick describes his most recent book negotiation. He got together a bunch of publishers on the call (they had all agreed to this before hand so weren't completely blind sided.). He then starts off at a LUDICROUS number and slowly starts counting down. Eventually someone blinked at a point 2-3x what they were willing to offer one on one. This high pressure situations ramps up the fomo (fear of missing out for my non-millennial friends) faster than a Friday night in high school. Eventually someone will blink and offer you a good price because they are worried that someone knows something they don't since the price is so much higher than they were willing to offer initially. This strategy only works when you a) are bargaining from an existing position of strength b) are able to get several similar buyers together in an auction setting and c) the negotiation is more transnational in nature and less about building a lasting relationship.

One important caveat. This should all be taken with a healthy dose of salt grains. I am early in my career and haven't exactly been negotiating international joint developments protocols in my free time. The most high stakes negotiation I face on a regular basis is figuring out where to go to dinner with my wife (we are one of those couples where the negotiation centers more around wanting the other person to decide than actually feeling strongly about somewhere in particular.)

That being said, each of these strategies really resonated with me and when I am negotiating the name for Mars colony 3, these will be the paradigms I lean on.

Podcast of the Week: The Tim Ferriss Show #341: Nick Kokonas

I love podcasts. They are my absolute favorite way to consume content. The great thing about podcasts is that they are the only form of content that gives you your time BACK instead of taking it away from you. Since you can listen to podcasts speed up and while you are doing something else, you are able to squeeze more hours into your day. I typically listen to 2-3 hrs of podcasts a day during my commute and while doing chores around the house. These podcasts are a great source of learning and give me the super power of having 27 hours in every day.

My favorite part of listening to podcasts, is sharing them with others! I thought it would be fun to start sharing my favorite podcast from the week with my readers. I’ll give brief overview of the podcast, topic/guest, and I will embed the podcast so you can enjoy it too! I am planning on doing a Podcast of the Week post once a week (surprise, surprise). Let me know in the comments what your favorite podcasts are and if you have any suggested shows for future weeks!

This first podcast is without doubt one of my favorite podcasts of all time. In episode #341 of the Tim Ferriss show, Tim interviews Nick Kokonas about hist story from commodity trader on the floor of the Chicago exchange to co-owner of one of the most successful high-end restaurant groups in the country, The Alinea Group. The thing I love about Nick’s story is that at every turn he questioned the status quo and tried to come up with how things SHOULD be done instead of just how they had always been done in the past. It is a refreshing mindset and a thoroughly enjoyable episode. Do not miss this one and do not be scared away by it’s hefty length, it is absolutely worth it!

Would you rather get rich or change the world?

As part of my entrepreneurship concentration in college I took a few classes on entrepreneurship and venture capital with a professor that had been both a successful entrepreneur and venture capitalist. I thoroughly enjoyed his brusque and brutally honest style (he was known to carry around a yellow football penalty flag that he called his “Bullshit Flag” and was he did not hesitate to throw it whenever people got a little too fresh with the truth). One of the common questions he would ask us to ponder is would you rather invest in an entrepreneur interested in getting rich or changing the world. Invariably whenever he asked this he would then have us raise our hands depending on our answer.

I was always in the minority (or sometimes the only one) that said they would rather invest in an entrepreneur that was trying to change the world.

His argument is that the world of venture capital is tough and that only the fittest companies survive. If an entrepreneur isn’t dead set on getting rich, they won’t prioritize growth the way that you, as an investor, need them too. A focus on changing the world to stop short of the best financial outcome when it is just over the horizon. My response was always that there are a ton of ways to accrue wealth in this life and that only entrepreneurs that are truly passionate about solving a problem in the world will succeed. I believed that the wealth would come from the offshoot of that success, just not as its primary driver.

Of all the things I learned in this class, it was this conversation that always stuck with me the most (though I doubt I will ever forget his bullshit flag either!).

Would you rather get rich or change the world?

This is a question that I have been pondering and discussing a lot recently as I have had the opportunity to work with founders that clearly come from both camps. There are a lot of strong arguments people make for supporting the team trying to get rich. They will act in alignment with our goals as investors. They won’t settle for a less than excellent outcome. They won’t get pulled in different directions by their altruistic goals.

And at the end of the day, I have to admit I agree with a lot of the get rich argument. It makes sense from the perspective as an investor with a fiduciary responsibility to their LPs. And anyone who knows me will tell you that I am as much of a free-market capitalism loving libertarian as the next guy.

But I can’t help believing that the best investments are made in founding teams that truly believe that it is up to them to change the world. Teams that have experienced the problem they are fixing personally and who genuinely think that if they don’t solve this issue, no one else will.

I want to invest in the next Elon Musk, who thinks that it is his personal responsibility to make mankind an interplanetary species, rather than the next Jeff Bezos, who saw the online trend before anyone else and took advantage of it to build one of the world’s most dominant businesses. Now obviously investing in either the next Musk or Bezos would be an incredible investment, but the choice is clear to me.

I want to invest in the dreamers that have a mission and a purpose permeating everything they do. I want to invest in the builders that believe that tomorrow will be better than yesterday and that no problem is insurmountable. I want to invest in the founders that will never give up because they can’t stand the thought of letting the problem they are trying to solve effect one more person.

I want to invest in people trying to change the world.

If they win, we all win.

An Introduction to Opportunity Zones

My wife and I are celebrating our 1-year anniversary this weekend with a quick getaway to somewhere yet-to-be-disclosed (I planned and surprised her with our honeymoon and now we plan to switch off for our anniversaries moving forward). As such, this week I will be doing a somewhat abbreviated post. Don’t let the brevity fool you though, the topic of Opportunity Zones is one that I am spending a lot of time researching and thinking about. This piece of legislation passed as part of the 2017 tax reform has some exciting implications for investors and low-income communities In the above video, Steve Glickman co-founder of the Economic Innovation Group (the lobby group that pushed for this legislation) outlines what exactly opportunity zones are at a high level.

(Side note: I read a very interesting article on why some of the measures of growing inequality and lack of financial prospects in this country may be overplayed that you may find interesting. My view is that there are definitely structural problems that need solving, but it requires a more nuanced approach than sometimes suggested. I think Opportunity Zones (OZs for the cool kids) can be that approach. Anyways, back to your normally scheduled running train of thoughts from inside of my head)

My understanding of how Opportunity Zones work on a high level (not tax advice):

Investors can defer taxes on existing capital gains by investing those gains into an Opportunity Zone fund for up to 9 years

If those gains are held in the fund for over 10+ years, the investor does not have to pay any taxes on the additional gain those funds have realized over the life of their investment

The purpose of this initiative is to spur economic development in emerging market areas within the US. The incentive is investment type agnostic so venture capital investors can take advantage of these incentives alongside other investors such as real estate and private equity. The IRS just released some very investor friendly initial guidance, but there are still some questions that remain to be answered.

If you want to learn more, below are some excellent resources that I have been using to get up to speed on the potential opportunity (come on you knew I was going to do it at least once. Be impressed I showed this much restraint).

Economic Innovation Group - The lobby group that pushed for the OZ legislation. Their site is a great resource for the latest developments for the program and also has some interesting resources (including an OZ map that is weirdly fun to play around with).

Hypothesis Ventures - A new VC firm that was formed with the sole intention of investing in opportunity zones. Their website is a great resources as well as their podcast and some of the press coverage they have been receiving

Upside - One of my new favorite podcasts highlighting startups outside of Silicon Valley (sound familiar). They have a great episode with the founder of Hypothesis.vc that is definitely worth a listen!

Venture Capital and the Red Queen

This past week I came across a fascinating concept in evolutionary biology called the Red Queen Hypothesis. The Red Queen Hypothesis proposes that organisms must maintain a perpetual state of adaptation and evolution, not only to gain a reproductive advantage against rivals from within their own species, but merely to survive in an ever-changing world filled with other constantly evolving organisms. The Red Queen Hypothesis paints evolution not as an inevitable outcome of generation after generation of survival of the fittest, but as a species-level arms race of life or death.

Evolutionary Biologist Leigh Van Valen developed the Red Queen Hypothesis as a potential explanation for why a species’ extinction rate is relatively flat over time. Under the core tenets of the theory of evolution, one would expect that as species evolve over time, the chance of them going extinct would diminish, but empirical evidence has shown this to not be the case. Van Valen named his hypothesis after the Red Queen from Lewis Carrol’s 1871 novel Through The Looking Glass (sequel to Alice’s Adventures in Wonderland). At one point in the book, the antagonistic Red Queen tells Alice that:

“Now, here, you see, it takes all the running you can do, to keep in the same place.”

Exhibit 1. The wily and cunning fox. Notice the hallmarks of an evolutionary predator. Pointed ears, sharp claws and a stylish three piece suit with occasion appropriate accessories.

Exhibit 2. The swift hare. Large ears have developed to be able to sense the slightest sounds. Evolutionary biologists maintain that the true reason behind the hare’s insistence on wearing gloves and proclivity to ask “whaddup, doc?” were lost a millenia ago.

This idea of running just to stay where you are is an apt metaphor for the necessity of an organism to constantly evolve just to maintain its current place in the evolutionary order. The most obvious example of this in nature also involves running. Imagine the perpetual evolutionary dance between the wily fox and the swift hare. The hare constantly evolves to become faster as the slowest hares are removed from the gene pool by the hungry fox. The inverse happens to the fox, with their slowest numbers dying out from not being able to get enough food to eat. This plays out as a balancing act of co-evolution where both foxes and hares will get faster and faster over time. If either species stops keeping pace in this evolutionary arms race, it will either die out or be forced to adapt in other ways. As long as both the fox and the hare keep at roughly the same pace, their relationship will remain locked in place.

The world of technology startups and venture capital has many of the hallmarks of the Red Queen Hypothesis. Incumbents and disruptors are often locked in a battle of the hare and the fox. As soon as either starts slowing down, their demise is relatively swift. Companies need to constantly be reinventing themselves to stay on top. This is easier said than done. If you look at the tech titans of 20 years ago, only Microsoft has been able to maintain its status as one of the leaders in the space (and even then it is no longer as dominant as it once was). It will be interesting to look back in 20 more years and see whether the Amazons and Apples of the world are able to maintain the current status they enjoy. Some might point to the incredible power that today’s incumbent companies have, but at one point it was similarly hard to imagine that seemingly invincible tech titans like AOL and Xerox would ever fall from grace.

Startups have a biological imperative to constantly be growing and innovating. If they don’t, they will die just as surely as hares would if foxes suddenly evolved to be born with jetpacks. The other day I saw a well-regarded venture capitalist compare startups who take venture funding to sharks. Sharks are only able to “breathe” by constantly swimming so that water passes through their gills and can be absorbed. Constant innovation is similarly the only thing that keeps startups flush with oxygen. You may argue about whether this is the way that things should be, but it is hard to argue with the fact that once a company gets on the venture train, it is exceedingly difficult to get off at the next station. As a founder, you should understand that an ability to evolve and adapt is table stakes. It is not enough to build one great product. You need to constantly and consistently be improving and building better and better products.

How can this be done? Are all companies doomed to fail at the slightest slip up? What can a company do to keep on innovating?

Luckily our world is in a constant state of change which means that there will always be new opportunities for companies that truly build themselves to constantly innovate. The path to constant innovation is surprisingly straightforward, but only an extremely small number of companies ever execute on it over the long term.

The first step is to create a diverse and high quality talent pipeline that will continuously refresh your company with new ideas and perspectives. A focus on diversity must start on Day 1, because if you, as a founder, don’t start focusing on diversity within your first 10 hires, it will be extremely difficult to start doing so after our first 100 hires.

The second step is to keep your eye on the horizon. Reinvest in yourself to stay on the bleeding edge of innovation. Don’t rest on your laurels and expect that what worked yesterday will work tomorrow. Always be on the look out for new opportunities recently enabled by social or technological change. If companies only tried to build upon what made them initially successful, Amazon would be the world’s best place to shop online for books (but nothing else) and Netflix would be the first place we would all go to rent our favorite DVDs through the mail.

The third step is to think for the long-term, without losing the ability to block and tackle over the short term. Apple is the master of this. They never fail to deliver on their quarterly objectives, even as they maintain a long-range focus on the next quarter century. Their obsessive focus on long-term planning has allowed them to build products that people will love to use today, even as they incorporate the building blocks of what their future products will be 10 years down the road. When Apple first built the fingerprint scanners into iPhones, they were preparing us for a day when our face would be the key to our most valuable data. If you pay attention, Apple has slowly but surely been incorporating more and more health and AR focused capabilities into their products. Don’t be surprised when new products with each of those categories at the forefront are released in the coming years.

The fourth step is to think based on first principles about the way things should be done, not the ways that they are done today. The insurance industry has been notoriously slow to embrace new technology and innovation. There are some structural advantages insurance companies have that make it a great sector to be a part of, but these same structural advantages allow them to sometimes forego evolution. In Columbus, we have seen the birth of next-generation insurance companies like Root Insurance and Beam Dental that underwrite risk based on measured activity, instead of age and demographic characteristics. Constantly ask yourself why things are being done a certain way and how should they work based on your understanding of people and available technology.

And that’s all it takes. Not so hard right? The difficulty comes in execution… and the fact that everyone else out there is going to be the fox nipping at your heels. Success is possible, but it won’t ever be easy.

Run fast.

Run hard.

Run hungry.

And you might just stand a chance.

How to Invest Like the Best of the Midwest for the Rest

I had the privileged of seeing Andy Jenks, Partner at Drive Capital speak last week at Ohio State’s Venture and Startup Summit. Drive are the big dogs in town with over half a billion dollars in capital and investments into some of the top companies in the Midwest. I really enjoyed Andy’s speech and thought there were some insightful nuggets in there that were worth sharing.

The Midwest startup ecosystem is flourishing right before our eyes…

Now this is something Andy and I agree upon! The Midwest has all the ingredients to be a successful startup ecosystem. High quality universities, low-cost of living, and a strong corporate base combine to form a potent cocktail for growing new enterprises. The Midwest is also slowly, but surely starting to get some startup momentum. Successful startups inject new capital into an ecosystem and unleash the next generation of entrepreneurs in that area. In 2013, ExactTarget was acquired by SalesForce for $2.5 billion. In 2017, CoverMyMeds was acquired by McKesson for over a $1 billion. In 2018, Duo was acquired by Cisco for over $2 billion. Acquisitions like these will seed the next wave of great startups in the region.

… but investors on the coast still have a bias against the region despite their claims to the contrary.

This was disappointing to hear, but maybe not completely surprising. Despite increased media attention and success story after success story, Jenks claimed that coastal investors are still not willing to give Midwestern startups a fair shake. The cynical part of me would call this blatant geographic bias. The more optimistic part would point to the fact that venture investing is a relationship business and being located closer to the startups you are investing into means you can better support the entrepreneurs you are partnered with. The truth probably lies somewhere in the middle. The fact is that if a startup wants to raise serious institutional money from the coasts, they need to have better metrics and more traction than a similar startup in the bay area or New York would need to raise the same amount.

Getting the most out of your board

I love this one. Andy mentioned that he tells all of the founders of boards he serves on to “give him homework.” I think this is a great mentality from a board member, but even more so I think this should be a mindset that all founders should adopt. You don’t have to spend much time in the space to see that unhealthy founder-board relationships are pretty pervasive throughout the startup landscape. Too often founders look at their boards in an antagonistic light. This is a recipe for disaster as founders begin to withhold information from the board and then by the time these issues surface, it is too late for the board to help. The best boards have a symbiotic relationship with a company’s founding team. The board’s purpose is to support and advise the founder, not hound them or tell them how they can do their job better. I love the accountability that assigning each board member a task to complete before the next meeting brings. I think this is a great way to keep your board aligned and engaged, while generating value for the company from the most knowledgeable, experienced, and well-connected people at the table.

Focus on the market first

One of the most interesting parts of the presentation was Andy’s discussion about how Drive develops their investment theses. Drive takes a very market-driven approach to investing. They spend a lot of time building what they call “market maps”. These market maps chart out all the different aspects of a particular market and help Drive determine how they want to attack a particular market and what sort of companies they would be interested in investing in. There is a debate in venture about what matters more, the market or the team. What Drive would tell you is that markets need to be big enough to support the sort of outsized return they need to generate on their successful exits. Proponents of the market first approach will also point to the fact that a good team in a bad market will not be successful, but a bad team in a good market may still be successful despite themselves. My response would be that the absolute best teams have the ability to build markets that never existed before. My personal view aligns much more closely to that of Peter Thiel’s strategy, find a niche that you can attack, build a defensible position, and then build the market from there. To be honest, I think that much of the debate depends on what stage you are investing in. For larger, later-stage shops like Drive, it makes 100% sense to focus on market sizes because when you are deploying hundreds of millions of dollars at a time, every company you invest into needs to have a market large enough to support a billion (or even multi-billion) dollar enterprise. When you are investing in the the earliest stage companies, I believe it makes more sense to invest in the best possible teams. The best teams will be able to pivot when others won’t and may even be able to build a multi-billion dollar market where one never existed before.

There are things we need to still do better on

One of my favorite parts of Andy’s speech was that it was relatively pragmatic in nature. A lot of the presentations around the Midwest startup ecosystem can take on a very ra-ra tone, which makes sense. The great companies being built here continue to be overlooked and it is important to bring attention to them and the growth of the region as a whole. However, as promising as the Midwest’s trajectory is, not everything is perfect. Jenks highlighted a few ways that we need to improve if we really want to take the next step towards being a bonafide startup ecosystem. He urged investors and entrepreneurs alike to aim higher, raise more, and attack bigger markets. I like this. I will be the first to tell you that venture funding is not for everyone, but if it is right for your company, you are joining a game of fastballs and home runs, not grounders to left field (is it weird how many baseball metaphors I use when I am not even a big fan of the sport? I need to start working in more soccer references. Something to think on…). I want to invest in companies working on big ideas. Capital B BIG ideas. I want to invest in companies working on solving world hunger, traffic, cancer, the melting ice caps, and water shortages. And I think that the Midwest is the ideal place to build these sort of companies.

We need only to dream a bit bigger.

The Globalization of Venture Capital: Is United States Innovation Falling Behind?

There was a story doing the rounds this week about a new Center for American Entrepreneurship study about the globalization of Venture Capital. CAE’s study showed that the United States’ share of global venture capital investment had fallen 20% in the last five years and 50% in the last 25 years. These statistics were framed with alarming rhetoric from both the tech media and the Center for American Entrepreneurship.

VentureBeat stated that this report should give Americans “cause for concern.”

Richard Florida, one of the leaders of the study, stated that “[he] thinks for the first time, the U.S. is truly in trouble.”

Much of the discussion around this report has represented similarly disheartening views of the outlook for innovation in the United States. Media sites and commentators have worried over America’s loss of “edge,” and forewarned of dark days ahead.

My response:

Are we really so insecure that our place in the global order is threatened by the United States only receiving HALF of the globe’s capital invested into innovation?

The United States represents approximately 4% of the world’s population. By any objective viewpoint we are significantly punching above our weight to receive over 12x our share of the world’s risk capital.

But Erik, what about the relative decrease in our portion of venture capital investments? Shouldn’t we be worried about investment into our country decreasing by 20% in 5 years?

Short answer: No.

Long Answer: This is why Intro to Statistics is required coursework. Venture capital investing into the United States has not decreased by 20%, the share of global venture capital received by US-based companies has decreased by 20%. The difference is incredibly important.

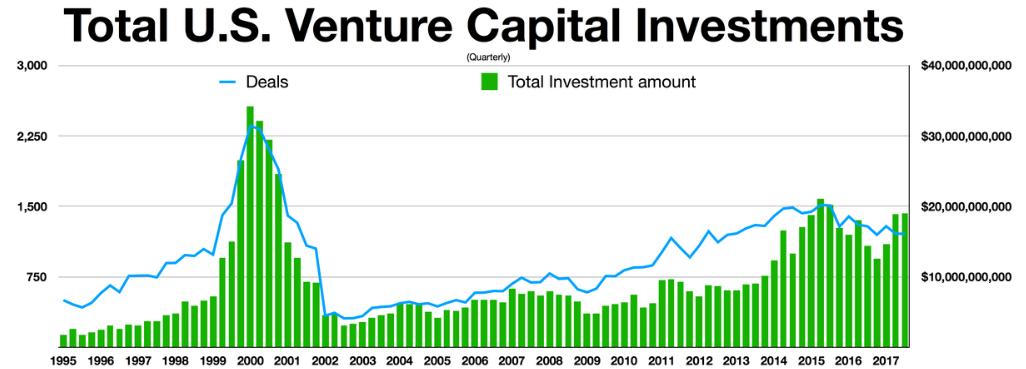

Via NVCA. As of June 30, 2018.

2018 is, in fact, poised to be the largest year for venture capital investment into US startups since the Dotcom crash. At the halfway point of 2018, about 3/4 of 2017’s total investment value has been deployed. This means that we are on pace for a potentially record breaking year (for discussion of whether this should even be something to be celebrated or not, check out last week’s post.) Yes, our piece of the overall venture capital pie is shrinking, but the overall size of the pie is magnitudes greater than it used to be. That is what matters most. Innovation is not a zero sum game, our ability to innovate is not hampered by China’s or India’s. In fact, it is the reverse. Increasing levels of global innovation create network effects which the United States can take advantage of to propel us even further.

It is short sighted and, frankly, close-minded to believe that the United States has some sort of divine right to be the innovation capital of the world. Innovation, by its very nature, is meritocratic. The United States’ shrinking share of venture capital dollars should be met with fanfare, not rumors of our impending demise. The rest of the world is catching up, and that can only be a good thing. More innovation means more impactful technologies that can improve people’s lives for the better. Where that innovation occurs is far less important than the fact that it is occurring, and if we are being honest with ourselves, there are many parts of the world that need ground-breaking innovation a lot more than the United States needs a new social media app.

We are not facing an innovation crisis in the United States. We are the pioneer of modern technological innovation and the rest of the world is starting to build up their own capabilities on the back of 80 years of the United States writing the playbook.

This is a good thing.

For everyone.

To suggest otherwise is both alarmist and misguided.

If you enjoyed this post and would like to receive others like it directly to your inbox, please subscribe at the top of this page. While doing so, you may notice a new “Pitch Me” tab. If you are working on an innovative idea or company, I want to hear from you. Use this tab to get in touch with me regarding what you are working on. I will review everything and respond within 48 hours.

The Big get Bigger: An Analysis of the Current Venture Climate

Figure 1. Via NVCA. As of Q2 2018.

Anyone familiar with the venture capital industry will know that we are in an investing and fundraising environment that is relatively unprecedented in the history of venture capital. The rise of “mega-funds” totaling sizes of up to $100 billion in the case of Softbank’s Vision Fund, has lead to deals at sizes that have never been seen before. Uber’s most recent $500m round lead by Toyota valued the company at over $70 billion dollars. The high-dollar amounts and the relatively frothy fundraising environment have instigated headlines ranging in size and shape but almost universally pessimistic as to the outlook of the industry. Some people believe that we are in a bubble the likes of which has not been seen since 2000. Others, especially LPs, Corporate VCs, and Growth Equity shops believe it is an excellent time to get increased exposure to the space. I did some digging into the data to try to find out exactly what is going on.

Here’s what I found.

We are a long way away from seeing Dot-com crash levels

Figure 2. Via NVCA

Some have compared the current venture climate to the Dot-com bubble of the early 2000s where companies could go public and double their value just by adding “.com” to the end of their name. Everything quickly came tumbling down and investors discovered that simply putting something on the internet was not a way to create lasting value. Despite high-valuation numbers, the current environment remains a far cry from the Dot-com bubble. As Figure 2 illustrates, the current climate is the outcome of an elongated period of sustained industry growth and demonstrates neither the hyper-acceleration of deals we saw in 1999 nor the crash’s sizable peak investment amount. If we are in a bubble, it will look very different when it bursts.

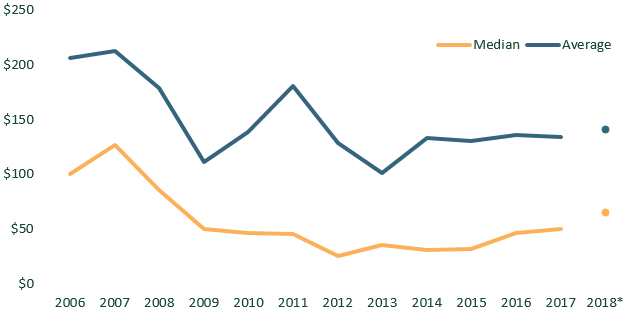

Fund sizes are not as big as you think they are

Figure 3. Via NVCA. As of Q2 2018.

This one surprised me and definitely flies in the face of the popular narrative. When looking at the industry as a whole, fund sizes are not meaningfully larger than they were a decade ago. What is important to notice though is how the spread between the average fund size and median fund size has expanded. This indicates that the absolute largest funds at the top of the spectrum are dragging the average fund size up as the median fund size has risen much more modestly.

But median follow-on fund size is increasing…

Figure 4. Via NVCA. As of Q2 2018.

…even as the time between funds shrinks

Figure 5. Via NVCA. As of Q2 2018.

These trends definitely show the frothy fundraising environment that firms are enjoying. Venture firms have been able to raise larger follow-on funds more and more often. This phenomenon is not unique to venture capital. I saw first hand at my prior job just how much of a desire there was from institutional investors to gain exposure to alternative asset classes. It will be interesting to see if these trends are sustainable as deals take an increasingly long time to exit.

Deals are take an increasingly long time to exit

Figure 6. Via NVCA. As of Q2 2018.

Told you so. The time to exit for venture backed companies has slowly crept upwards over the past decade. The exception to this is companies exiting through a public offering where time to IPO has stayed largely flat and is even slightly down versus a peak in 2012. This speed to IPO makes sense in light of the many venture backed companies that have had their shares publicly listed over the past couple of years including StitchFix, Snap, and Shopify (those are just the high profile ones starting with S! Seriously though do you think there is something there…? I’ve decided that I am going to name my future company Soogle.)

Corporate Venture Capital is getting in on the fun

Figure 7. Via NVCA. As of Q2 2018.

One of the hot takes on the current environment I have heard a couple of times now is that “the growth of corporate venture programs is a clear sign that we are in a bubble.” This seems pretty difficult to say with any measure of confidence due to the fact that we have been through a grand total of ONE venture capital bubble before, but it is hard to ignore the growing leverage over the space that CVCs are enjoying. I found it very interesting that the percent of deals that have involved corporate venture arms has stayed relatively flat, even as the overall percentage of deal value has increased by approximately 50%. Corporates are putting significantly more capital to work as they take more ownership in bigger rounds.

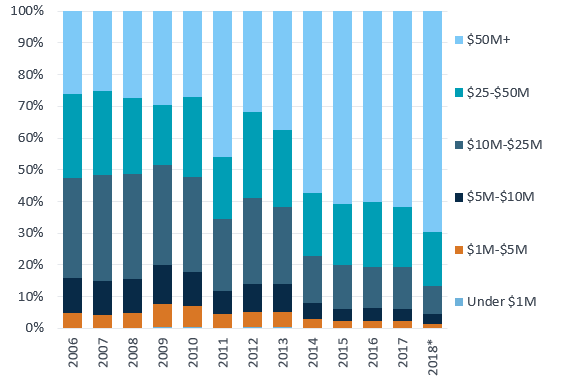

Deals are bigger than they used to be

Figure 8. Via NVCA. As of Q2 2018.

Speaking of bigger rounds. This chart of median deal size does a great job of illustrating the growth of later stage rounds compared to early rounds. As you can see, the driver behind the growth in deal size really is later stage rounds. This makes sense. There has been an explosion of both corporate VCs and Growth Equity shops to go along with larger mega funds. All of these groups have large funds that need to deploy large amounts of capital at once.

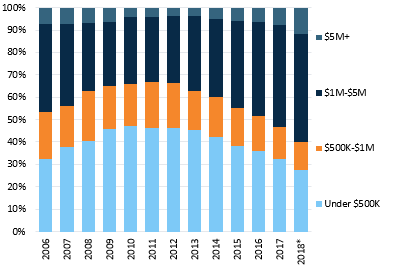

Even within Late stage, deal sizes are being driven by the top of the curve

Figure 9. Via NVCA. As of Q2 2018.

This one is very interesting. This chart shows dollars invested into late stage rounds by deal size and does a great job of demonstrating that even in the later stages, the biggest deals are taking up a larger and larger portion of the pie.

Valuations are getting more and more expensive

Figure 10. Via NVCA. As of Q2 2018.

Figure 10 shows the increasing pre-money valuations that we are seeing today. What is causing this growth in valuation? The relationship between deal size and valuation can be a little bit like the chicken and the egg. Are deals bigger because valuations are higher and firms need to deploy more capital to maintain their targeted ownership? Or are valuations higher because there is a glut of capital and entrepreneurs are getting more capital for less ownership in their company? Given the similar trends in private equity, I tend to believe it is more of the latter. I believe low interest rates have caused large institutional LPs to allocate more capital towards alternative assets in search of yield. Suddenly managers had significantly higher fund sizes and needed to allocate more dollars to each deal. Entrepreneurs (and investors!) don’t want to be over-diluted and this has pushed up valuations as they are able to command higher valuations for the higher deal sizes.

Seed deal size are increasing (even if relatively less than later stage)

Figure 11. Via NVCA. As of Q2 2018.

Seed deals are showing a clear trend of getting bigger too. More deals are being done with larger round sizes. Hunter Walk has a great post about how seed is no longer a discrete round, but now more of a phase where companies may need to raise multiple rounds at higher and higher valuations before being ready for an institutional Series A. I suspect this is one of the big drivers for increasing seed sizes (on top of the macro-trends growing round sizes across the industry).

Angels are surprisingly disciplined (or more likely they are being shut out of deals)

Figure 12. Via NVCA. As of Q2 2018.

Angel investors are not following the same trends as institutional investors. Figure 12 shows the growing discrepancy between angel and seed median round size. There are a few potential explanations of this. 1) Angels are maintaining price discipline (maybe out of necessity?) where others are not. 2) Friends and family rounds are not growing the same way other rounds are since they are not exposed to the same institutional LPs as funds are (could be). 3) Angels are being squeezed out of more expensive seed deals. My hunch is that it is likely a mix of all of the above, but if I had to put the blame on one thing, it would be angels getting squeezed out of rounds. For better or for worse, Entrepreneurs would generally prefer institutional investors to angel investors, with the abundance of capital being thrown around today, my guess is that angels aren’t getting into deals because there is simply enough interest from institutional investors to close out rounds. This one is very interesting to me because we are still seeing heavy involvement from angel investors in the deals we are executing at Rev1. Maybe we chalk this one up to the coasts?

So what did we learn from my deep dive? Digging into the statistics showed some of what we already knew, but it also revealed some insights I wasn’t expecting. The largest funds are getting bigger, deals are getting bigger, and valuations are getting bigger. Venture Capital firms are raising larger follow on funds at a more rapid clip than ever before. There are; however, some things we found that fly in the face of the popular narrative. Angel investors are not being effected (perhaps unsurprisingly) by some of the same trends effecting the industry at large, fund sizes are not meaningfully larger when you look at the industry as a whole, and the current environment has not yet reached the heights of the Dot-com bubble.

It is dangerous to rely too heavily on historical events as a sign of things to come. As with most things, the truth is somewhere in the middle.

How I got a job in Venture Capital

Ever since I started in my new role as an Analyst at Rev1 Ventures, I have been intending to write a post detailing my experience trying to break into the world of venture capital. VC is a notoriously difficult sector to make your way in to, especially junior roles for someone only a couple years out of college. A common refrain that you will hear during informational interviews is that there are more professional baseball players than there are venture capitalists. This fact may be overblown (and certainly compares apples to oranges), but it does demonstrate just how difficult it can be to get into the field. Many arguments can be made as to exactly why this is, but at the end of the day, it boils down to a lot of people vying for relatively few open positions.

I was able to make the transition because I made a plan and executed on that plan. There are things I would've done differently, but I think the fact that I was able to make it to final round interviews at 4 different firms demonstrates that my planning was effective.

One of the first things you learn as you start exploring a career path in VC is that the world of venture is filled with people that are willing to take time to help someone along their journey. Hopefully, some of the insights I have learned can be a resource for other people trying to make their way into the big leagues.

Fake it till you make it

The biggest piece of advice I can give to someone trying to get into the world of venture capital, and the place where I think I did the best job in my process, is to fake it till you make it. This means that even before you start working in VC, you should start acting like a venture capitalist. Working in private equity at The Carlyle Group, I knew I was in a related field and at a blue-chip firm that would help get my foot in the door (which it definitely did, but I was on my own past that point), but I also knew that my day-to-day at Carlyle was nothing like what my day-to-day would be like working at a venture capital firm. At Carlyle, I was dealing with billion-dollar transactions that involved decades-old companies, compared to early-stage venture capital where companies may or may not even have a product in the market and any financial records are slim at best. This meant that I had to take it upon myself to demonstrate that I had what it took to be successful in venture.

You are reading the first way I did this. I started this blog for a variety of different reasons, but one of the main ones was so that I could build a "thought-record" for recruiting firms to look at and see that I had put time and effort into thinking critically about startups and the tech ecosystem. My write-ups on specific startups and my sector thesis deep-dives also gave me something to talk about in interviews. This may seem contrived, but if there is one piece of advice you take away from this post, START A BLOG. To be fair, it doesn't have to be a blog per se, but if you are interested in getting into the world of investing in startups, you need to start creating some sort of content that demonstrates you have spent time thinking critically about, you guessed it, investing in startups. (sidenote: I think this advice is applicable for anyone looking to change fields. Get out there and start creating content around where you want to GO, not where you are right now) I chose to blog because I had some limited (and angst-ridden) experience blogging in my high school days, I wanted to get better at writing, and, as a fan of many blogs, I felt like I had a good idea for what other readers would enjoy. Content creation takes work and commitment. No doubt about it. Before you toss aside this idea as not being worth the effort, you should know that the other analyst that I work alongside at Rev1 also started a blog as a way to help get into the industry. Must just be a coincidence...

The other way that I started acting like a VC was through angel investing. Now, I do not have the capital to qualify as an accredited investor (generally a requirement for angel investing), but I am fortunate enough that my father does and was interested in trying something new (he is in private equity, so investing isn't new, but investing in tech startups was). We read Angel (a book about angel investing by one of the best angels in the business), joined angel syndicates on sites like AngelList and Funder's Club, and were off to the races. I helped my dad analyze startup investment opportunities and was able to practice doing some of the things I now do in my job such as writing investment memos, developing front-end deal flow, and portfolio management. This experience of actually practicing some of the skills that I hoped to one day be performing professionally was absolutely invaluable. It gave me something to talk about in interviews and I believe it helped me to stand apart from the crowd of other would-be venture capitalists. I was lucky that I was able to get some exposure to this world by working with my dad, but you can still get this practice without a connection to an accredited investor. Sites like SeedInvest and WeFunder offer even unaccredited investors opportunities to invest in startups. You actually don't even need to make investments. You can sign up for these sites and just look at deals without making any actual investments. Maybe start a shadow portfolio where you track what investments you would've made and how they performed. If you see something especially promising that fits a firm's investment thesis, send it to the attention of a VC you have met through networking. It might not be something they invest in, but if it is thoughtful and fits their firm's investment guidelines, I have never met a VC that wouldn't be impressed.

Whenever you are trying to make a career change into a field different from where you have tangible experience, you need to take it upon yourself to find a way to get exposure outside of your normal working hours. This is especially true in as competitive and nuanced a field as venture. Come up with a way to demonstrate that you are being thoughtful about whatever space you are interested in jumping into. Go to industry-specific events and meetups and connect with people that are actually doing the work you want to be doing. However you want to approach it, faking it till you make it will give you a leg up on landing the role you want.

Take advantage of the resources that are out there

There are a ton of excellent resources on venture capital that you should be immersing yourself in if you want to work in the space. Below I have listed a few of my favorites.

Podcasts

20 Minute VC - An awesome and bite-sized way to get smarter on the "wonderful world of venture capital". In each episode, Harry Stebbings interviews a venture capital investor or startup founder in about twenty minutes. I really enjoy this podcast and Harry is a super nice guy that was kind enough to be a resource to me during my job search.

Invest Like The Best - This podcast hosted by Patrick O'Shaughnessy is my absolute favorite podcast. It covers a wide variety of topics including investing of all types, as well as ways to lead a better and more productive life. The podcasts on venture capital are a great resource, but my favorite episodes are the ones that have nothing to do with investing at all. Patrick also has done a great intro to crypto series that is an awesome first step into that world.

How I Built This - This NPR podcast with Guy Raz is a super interesting and entertaining exploration about how entrepreneurs and business leaders built the companies they are famous for. Not every company explored was a venture-backed startup, but I have found interesting insights about the entrepreneurial journey in every single episode.

a16z Podcast - Andreessen Horowitz's podcast is my favorite firm-sponsored podcast. They mostly showcase topic or sector deep dives from various a16z speaker events. Definitely a great way to get smarter on specific sectors.

Angel: The Podcast - Jason Calacanis' podcast accompaniment to his previously-mentioned book on angel investing. Excellent interviews with both angel and institutional venture capital investors. Jason hasn't done an episode of Angel in a while, but he is also the host of This Week In Startups which is very good.

Websites

avc.com - The definitive venture capital blog by the grandmaster of venture capital, Fred Wilson. Fred publishes a new blog every single day and is a surefire source of wisdom about both life and investing.

John Gannon's Blog - The go-to source for anyone trying to break into venture capital. John's site lists helpful resources as well as a constantly updated source of open positions at venture capital firms.

TechCrunch - Cliche I know, but if TechCrunch is my favorite of the big tech news sites (others being VentureBeat, Recode, Hacker Noon etc) and somewhere I check at least once a day to get a view of what is going on in the ecosystem at large.

Feld Thoughts - Brad Feld of Foundry Group is another one of the big-name investors in the space and his blog is a great resource on the ecosystem. He has also written some must-read books for anyone interested in venture investing like Venture Deals.

Newsletters

StrictlyVC - A venture-only daily newsletter that covers the biggest stories and latest investments in venture.

Axios Pro Rata - Dan Primack's daily blast of the latest news in business and politics.

Fortune Term Sheet - Another great newsletter written by Polina Marinova that covers a wide swath of the latest news in business.

Network your socks off

Does networking matter?

Yes.

Moving on.

But seriously, networking is a key part of any venture capital job search. The reality is that at most firms, networking will be a relatively significant aspect of most junior roles. If you can't network your way to decision makers at firms, how will you ever be able to network your way into meeting the best and brightest founders? To be honest, networking did not come naturally to me either when I first started my process. When I thought of networking, I thought of the overly-eager undergrad business students that would suck-up to anyone and everyone. I thought I was better than that. But I was so wrong about what exactly networking really was. It finally clicked for me when one of my colleagues described networking as meeting new people and hearing about their stories. I am an outgoing guy that enjoys meeting new people and making new friends and thinking of networking through this new lens helped it to really click for me and turned it from something I looked down on (and if I am being honest was anxious about doing) into something that I actually enjoyed. Now it is not all rainbows and butterflies. It is a skill that you need to practice like any other and it can be hard work. But like other skills, you will improve on it as you do it more and more. Networking through informational interviews with current venture capitalists is a great way to expand your network, learn more about specific firms/sectors of the venture ecosystem, and get your foot in the door.

Getting into venture isn't solely about networking, but it is an important aspect of any job search. For reference, 3 out of the 4 final round interviews I had with firms came about because of networking. BUT I ended up taking a job at the one firm where the opportunity came from me responding to a job-listing online. I think my experience is a great demonstration of just how important networking can be, but also how it isn't the end all be all.

Be flexible

Have you gotten the impression of how difficult it can be to make it into the industry yet? If I have not made it clear, let me do so again. Something something more baseball players than VCs something something small number of job openings something something a lot of people trying to get into the space something something 4 partners for every 1 junior level person.

You get the picture. Unless you have been part of a successful start-up, it will be difficult to get hired as a junior level person in the space. A way that you can mitigate this difficulty somewhat is by being flexible.

This doesn't mean apply for anything and everything in the space (though that is a legitimate strategy). Instead, pick one or two characteristics that are really important and be flexible on others.

I was very certain that I wanted to work at an early stage pre-seed/seed firm. I wanted to work with companies at the earliest level and really get in the weeds working alongside entrepreneurs. Because early-stage was a must for me, I decided to be more flexible on other things like where the firm was located.

Let me tell you, when I started my search a year ago, I did not expect that I would be writing this blog post from Columbus, Ohio! Being flexible will open up more opportunities for you and you just may end up falling in love with a place you never expected like my wife and I have with Columbus!

Why VC

Now that I have given you my playbook for getting into VC, you should step back and ask yourself if this is really the sector you want to be in. I can personally attest that it is not as glamorous as Techcrunch headlines would cause you to believe. There is a ton of hard work and grinding. The feedback loop for success is very long and for failure it is jarringly abrupt. If you are motivated strictly by financial upside you are better off going to Wall Street.

But for the right kind of person it is absolutely awesome!

I love what I do. I believe venture capital is a service industry whose customers are your founders and I love working alongside brilliant and motivated entrepreneurs to build game-changing companies. I am excited to go into work every day and gone are feelings of anxiety on Sunday nights. I love getting up to speed on new companies and learning about technologies that I didn't even know existed the day before. I love creatively solving problems and brainstorming ways for founders to run through the walls in their way. I love helping to build an ecosystem and I love working alongside people that are just as passionate as I am.

If venture still sounds like the place for you, give me a call (or reach out to me on twitter).

I'll be your first informational interview.

There's a Fungus Among Us: Fungibility in the Digital Age

Fungible.

What a weird word.

From the Latin fungibilis which means "to perform". A fungible good is something that can be replaced by an equal amount of something else without any loss of value or performance. Basically, an ounce of gold is an ounce of gold is an ounce of gold. It generally doesn't matter where the gold came from or what it used to be before it was melted down because all gold is fungible with all other gold. Most commodities (Oil, Gold, and my personal favorite lumber. Lumber deserves its own blog post at some point. Fascinating material from an investment perspective. The only major commodity that is self-replenishing, but I digress) are fungible goods as well as many consumer (Tommy Bahama Shirts) and digital goods (iTunes songs). Stocks are also a great example of a fungible good.

Fungibility is not a hard and fast rule though. Take my Tommy Bahama shirt example. Fungibility depends on how specific you get with the product. Shirts are non-fungible. Shirts come in different styles and cuts. They are made from different materials and some will keep you warm while others will show off the tattoo you regret from spring break in Cancun. Once you drill down a little bit deeper shirts become fungible. Every ridiculously overpriced Baja Batik Camp Shirt, in theory, is equivalent to every other ridiculously overpriced Baja Batik Camp Shirt.

Make sense?

What isn't a fungible good you ask?

Non-fungible goods are goods that can not be substituted while maintaining their value or production. Artwork is the classic example of non-fungible goods (despite what uncultured dolts like me may sometimes believe). Other common examples include people, land, and events. Nonfungible goods can often be expensive because they are in some way unique.

Easy right?

Not so fast.

The relatively straightforward paradigms of fungibility that we have become accustomed to are quickly being turned on their head by the advent of blockchains and other distributed ledgers.

Most crypto assets are fungible. They were designed this way so that they could be used as a means of value exchange. Bitcoin, Ether, Litecoin, and other major cryptocurrencies are all fungible goods. However, there are some crypto assets that have been specifically designed to be non-fungible. These appropriately named Non-Fungible Tokens (NFT) are unique from every other NFT. They signify ownership of a discrete and unique asset. The first widespread use of NFTs was in the popular CryptoKitty game (which I wrote more about here). CryptoKitties were unique digital pets with verifiable ownership. This was made possible through the use of NFTs on the Ethereum blockchain.

Non-Fungible Tokens have some very interesting potential use cases. They can be used to signify ownership of digital goods in a way that was never possible before. When you used to purchase music off of iTunes (so quaint I know), there wasn't any real way to show ownership over the songs you purchased. You'd purchase Sk8r Boi (really?) for $0.99 and you would get access to listen to the song to your heart's content. Your copy of the song was the same as everyone else's copy of the song. There was nothing traceable about it and no way to say who it really belonged to. This is what has made piracy of digital assets so notoriously difficult to combat against. It is very very difficult to definitively says who owns what and where a copy of a digital good came from.

Non-Fungible Tokens could change all of this.

Built on the blockchain, NFTs could signify definitive ownership of digital goods. We will know who purchased the good, who has owned it since, and who is the current holder of it. This ability to create digital scarcity is game-changing for digital assets like music, collectibles, and artwork.

On Valentine's day of this year, a piece of digital artwork, the Forever Rose, sold for $1 million to a group of 10 collectors. The Forever Rose exists on the Ethereum blockchain in the form of ROSE tokens that the owners hold. These tokens are technically not NFTs since they can be exchanged for each other and they each represent a portion of ownership in the digital piece of artwork (pictured at the top of this post). They are a representative of fungible artwork. The Forever Rose is a provocative example of the power of blockchain and token technologies and a glimpse into the future of what digital asset ownership could look like.

Red, White, and Blues

Photo by Aaron Burden on Unsplash

It is the 23rd of July and I am writing a post about Independence Day. Better late than never I suppose. The truth is that I started this post around the beginning of the month, but it was something that took a lot of time as it was important to me that I got it right.

Something about the 4th of July has always made me stop and think. I don't know if it is the fireworks, the flags, or the hot dogs. Maybe it is the fact that the broad brush strokes of Independence Day never change year to year, which serves as a great measuring stick for how much my life has.

This year there was a lot to think about. If you were to listen to the media and your Facebook feed, things would appear like they have never been worse. Partisan politics, trade wars, and children being ripped out of their parents' arms are just a few of the negative images that you would get blasted with if you were to so much as glance at a newspaper stand (do those exist anymore) or flip on the news. Things seem pretty bleak. For the first time, optimism among Americans under the age of 35 is less than that of people 55 or older.

But I don't believe that things are as bad as they seem. The 24-hr, commercial fueled news cycle is in the business of sales, and unfortunately, drama sells more than optimism. It is important to remember that things are rarely ever so bleak as the media makes them out to be (nor are things ever as perfect as your friends' Insta stories make them appear). That's why during times like this, I like to take a step back and think of everything that is going right! Here are some reasons to be optimistic about America.

The Revitalization of Small-Town America

Rumors of the demise of small-town America have been greatly exaggerated. The state of our nation has people very worried. The difficulties and divides facing our country are very real. Partisan politics and national outrage dominate the headlines of the day. Cultural, ethnic, and socioeconomic divides seem to be deepening. A 2016 study by the Atlantic found that only 36% of Americans thought the country was headed in the right direction.

Dire as things may seem, there is a different story going on in local communities across this country.

In the same Atlantic poll, two-thirds of Americans said that they were satisfied with their own financial situation and 85% said that they were satisfied by their position in life and their ability to pursue the American Dream. It is not a stretch to believe that sentiments likely have improved over the past two years with the economy the strongest it has been over the past 9-year expansion and with the jobless rate near 20-year lows and wages growing in step. This dichotomy between national and local sentiments is indicative of the resilience of America and our local communities. We may fight and kick and scrape at the national scale, as we segment ourselves by political affiliation, sexual orientation, race, and any differentiating factor we can find, but spend some time walking around main street America, and you will find that people treat each other as neighbors. They treat each other with respect and kindness. The media and our technology have allowed us to dehumanize one another, but at the micro level, we still see each other as human. Two people that may yell and scream at each other over social media are happy to help each other carry in the groceries in the real world.

I have been fascinated by the story of James and Deborah Fallows. The Fallows are journalists that have time and time again upended their lives to follow the biggest story of the day. They spent the 90's following the rise of tech giants like Microsoft and Amazon while living in Seattle. During the 2000's they lived in China and were there to witness firsthand China's economic explosion onto the world stage. In recent years, they have turned their eyes on small-town America where they embarked on a multi-year journey to visit small towns across the country and try to understand what is happening in everyday American communities. Their findings are that the state of our union is much healthier than would appear to outward observers. In their travels, they attributed these local revitalizations to the following drivers.

Civic Governments - Polls have found that while only a quarter of Americans believe that the national government is doing the right thing, as much as three-quarters of Americans believe in the steps that their local governments are taking. The Fallows observed this first hand across an array of communities of differing ethnic and socioeconomic backgrounds. They believe that these rejuvenated local governments are caused by the increasing quality of local government workers as well as the rise of technologies platforms which allow for easier interaction and adoption between governments and their constituencies.

Immigration - The Fallows found that despite the increasingly vitriolic national rhetoric around immigration issues, cities that were actually acting as the landing ground for new immigrants were doing an exceedingly good job of integrating them into their communities. Medium-sized cities that take in many of the refugees coming to this country have celebrated them and now immigrants make up a vital and impactful part of these diverse communities.

Talent Dispersal - There is a growing trend of highly skilled, highly educated workers moving and returning to small towns across the country. People are tired of brutal commutes, high costs of living, and status-obsessed cultures of our major coastal cities. As someone that is a part of this phenomenon, I can confidently say that my wife and I are loving our choice. People are noticeably more warm and friendly in Columbus than they were in DC and there is a real sense of community that you can get in a smaller town than you would ever get in a big city. Cities like Columbus are big enough to have a ton of things to do and all the modern amenities you could ask for, but small enough to maintain a community identity and avoid issues that bog down big cities like traffic and skyrocketing rent.

Schools - Our education system has issues and in many places lacks resources, but small town communities are developing creative solutions to this problem. An emphasis on community colleges and trade schools helps to equip people for fulfilling careers without the overwhelming financial burden of attending a traditional 4-year institution. College is not for everyone and small towns are leading the way in rethinking what a more flexible and inclusive system of higher education could look like.